Power of Sale in Ontario: What It Means When a Private Lender Comes After Your Home

Served with a Notice of Sale? Don’t panic-file.

By the time most of these files reach my desk, it’s already over. I’m a Licensed Insolvency Trustee in Ontario, and the power of sale has usually run its full course before I ever hear the debtor’s name. The house is sold. The debtor has left the building. What’s left is a letter telling them how much they still owe — because the sale proceeds didn’t cover everything.

This article is written for homeowners, but not for homeowners alone. If you are a lawyer, accountant, mortgage broker, realtor, financial advisor, or another professional advising someone who is facing a power of sale, or who may be heading toward one, what follows is written for you too. The earlier you understand how these proceedings unfold, the more you can do for the client in front of you.

From that vantage point, I often find myself wishing I could turn back time. Reading the file, I’ll see it: the debtor’s lawyer may have missed this item, or that one. It comes with special meaning for me, because in another life — many years ago — I was that lawyer, giving clients advice and special handling before things ever got this far.

So if you’re reading this earlier in the story — a Notice of Sale just in hand, wondering what to do — you still have time others didn’t. If a bankruptcy or a consumer proposal is right for you, that’s something I can help with. For those considering that route, it may help to understand what really happens when you meet with a Licensed Insolvency Trustee. But only as an absolute last resort. Before you get there, read what follows with due care.

What is power of sale?

Power of sale is a mortgage lender’s right to sell your home if you fall into default — without first going to court. In Ontario it’s governed by the Mortgages Act, R.S.O. 1990, c. M.40. The lender doesn’t sue you, win a judgment, and then seize the house. It relies on a remedy written into the mortgage and the statute, and it moves on its own timetable.

That’s what makes it fast — and why it catches people off guard.

What is a Notice of Sale?

A Notice of Sale is not a lawsuit, a judgment, or a seizure of your home. It’s a procedural step: the formal default warning a lender must serve before it can exercise power of sale. It doesn’t transfer title or, on its own, create a new debt. It’s the lender saying, in the form the law requires, “you’re in default, and here’s what happens next.”

There’s an important corollary the panic tends to hide: if you’ve only just been served, the process is not finished. A redemption window is still open — meaning there is still time to cure the default or weigh your options.

The statute sets hard minimums. Under s. 32 of the Mortgages Act, the Notice can’t be given until the default has continued for at least 15 days, and the sale can’t be made until at least 35 days after the Notice is given. (How the Notice must be served — personal service or registered mail — is set out in s. 33.)

The private-lender angle: short-term private and MIC mortgages — 12-month terms, high renewal and default fees — are often built to reach this trigger fast.

The Power of Sale Process in Ontario, Step by Step

How does power of sale work in Ontario? It follows a set sequence, and knowing where you are in it tells you how much room you still have.

- Default occurs. A missed payment, a failure to renew, a broken term — the mortgage falls into default.

- Notice of Sale is served. The lender can’t give it until the default has run at least 15 days (s. 32).

- The redemption period runs. The sale can’t be made until at least 35 days after the Notice (s. 32). During this window you can still cure the default — pay the arrears and costs — and stop the sale.

- The lender becomes entitled to sell. If the default isn’t cured in time, the lender may proceed.

- The property is marketed and sold.

- Sale proceeds are applied to the mortgage debt, interest, and the lender’s costs.

- Surplus or deficiency is addressed. Money left over goes back to you; a shortfall becomes a debt the lender can pursue — more on that below.

One feature of the process protects you while the window is open: once a Notice of Sale is given, the lender generally can’t launch a separate court action on the mortgage or against the property without leave of a Superior Court judge (s. 42). The law keeps it to one lane at a time.

One practical point: the redemption figure isn’t just your missed payments. It includes the lender’s interest and costs, which keep accruing while the clock runs. Who your lender is can make a real difference to how fast that figure grows — something we come back to below.

Power of sale vs foreclosure: what’s the difference?

People often use these two words interchangeably. They’re not the same thing, and the difference matters to you.

With foreclosure, the lender goes to court to take title to your home. The property becomes the lender’s. Because the lender takes the asset, it generally gives up the right to come after you for any shortfall — it has taken the house in satisfaction of the debt.

With power of sale, the lender doesn’t take title. It sells your home to a third party, applies the proceeds to what you owe, and — if there’s a shortfall — can still sue you personally on the mortgage covenant for the deficiency. You can lose the house and still owe money.

In Ontario, power of sale is the dominant remedy, for two reasons that both favour the lender: it’s faster, because it doesn’t require a court order to proceed, and it keeps the deficiency claim alive. That second point is the one that follows borrowers long after they’ve moved out — and it’s where my work as a trustee usually begins.

How private and MIC lenders use power of sale

Before going further, two terms worth defining plainly.

A private lender — or private mortgage lender — is simply a mortgage lender that isn’t a bank or credit union: a single individual with money to lend, a small mortgage firm, or a pooled fund. They aren’t regulated the way banks are, and they lend where banks won’t.

A MIC — a Mortgage Investment Corporation — is one common version of this: a company that gathers money from a group of investors and lends it out as mortgages, usually the higher-rate ones that don’t fit a bank’s rules. The investors earn the interest; the borrower pays it.

These lenders aren’t villains. They fill a real gap. When a bank turns a borrower down — self-employed income, a bruised credit score, a property the bank won’t touch — a private mortgage lender or MIC will often still say yes. But that “yes” comes at a price, and the price is built into the structure of the loan.

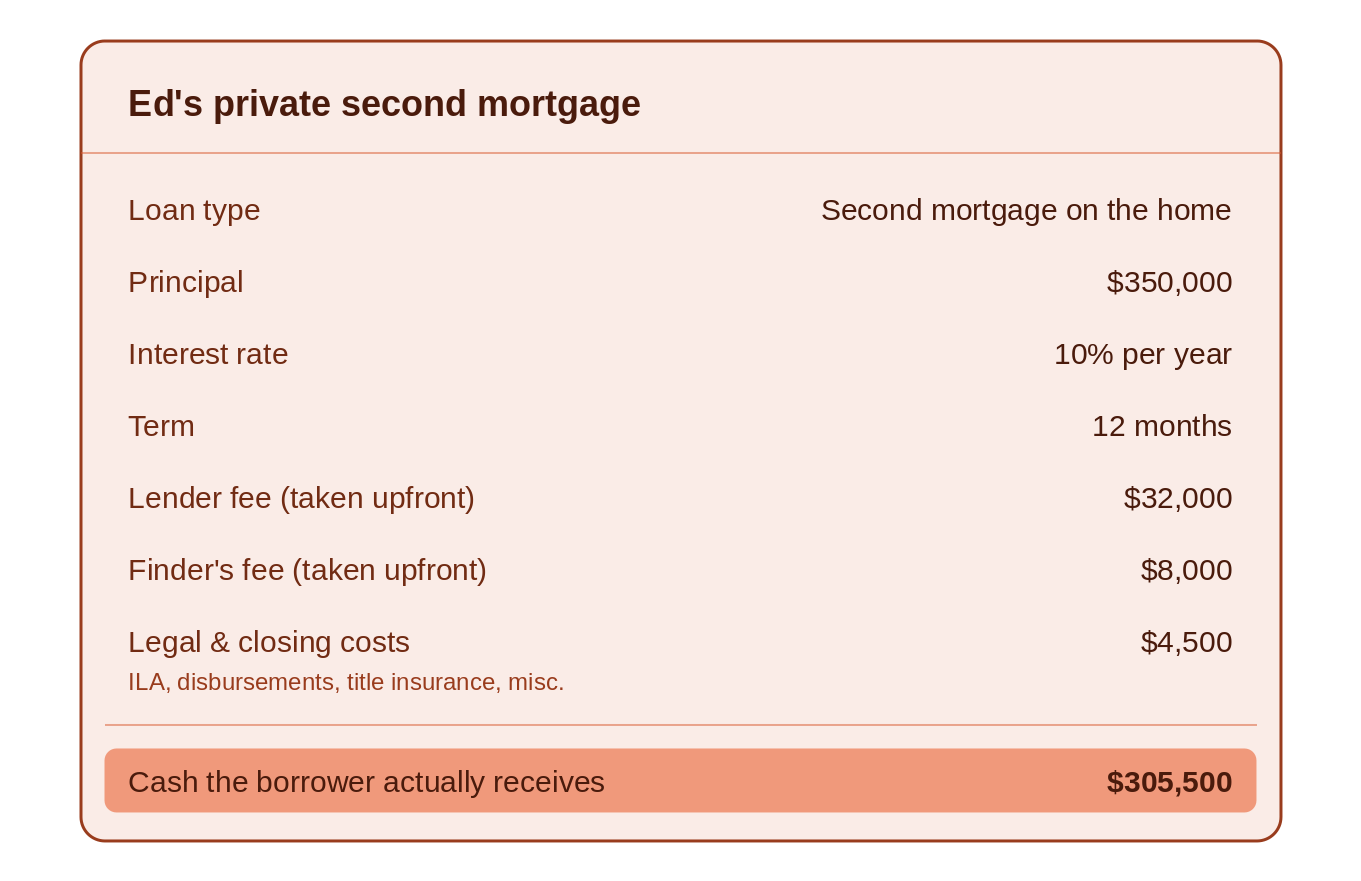

Meet Ed Paymaster — a private lender. A borrower the banks have turned away comes to Ed needing money, and Ed offers a second mortgage on the home. Here are the terms:

On paper, Ed’s loan looks expensive but survivable: 10% on a $350,000 mortgage. Ten percent is a number most people can picture and, under pressure, talk themselves into. But what’s advertised at an expensive-but-perhaps-manageable 10% costs far more than that simple stated figure. The 10% is charged on the full $350,000 — even though $44,500 in lender fee, finder’s fee, and legal and closing costs is taken off the top before the borrower sees a cent, so only $305,500 actually arrives. The borrower pays a full year’s interest on money they never received, on top of fees that are a second loan in all but name.

And the costs the borrower can’t see at signing push it higher still:

- a default rate — often 17% or more — that kicks in the moment a payment slips;

- a renewal fee, frequently equal to the original lender fee, if the loan isn’t repaid at the 12-month mark; and

- enforcement charges — notice of sale, statement of claim, possession fees — added straight onto the balance.

And Ed’s terms aren’t the worst of it. Depending on how distressed the borrower is and the situation they’re in, I’ve seen terms considerably more expensive than these. Rates and fees like Ed’s are not untypical when someone is borrowing to pay off an earlier private loan from a position of distress — the point at which few lenders will advance anything at all. These deals are usually arranged through a mortgage broker, drawing on the private lenders within that broker’s own roster of clients. By the time a borrower reaches this rung of the ladder, the choice isn’t between a good loan and a bad one. It’s between a bad loan and nothing.

When facing a Notice of Sale, homeowners are often approached by people offering quick fixes or guaranteed solutions. Understanding common debt consultant pitfalls can help you evaluate those offers more carefully.

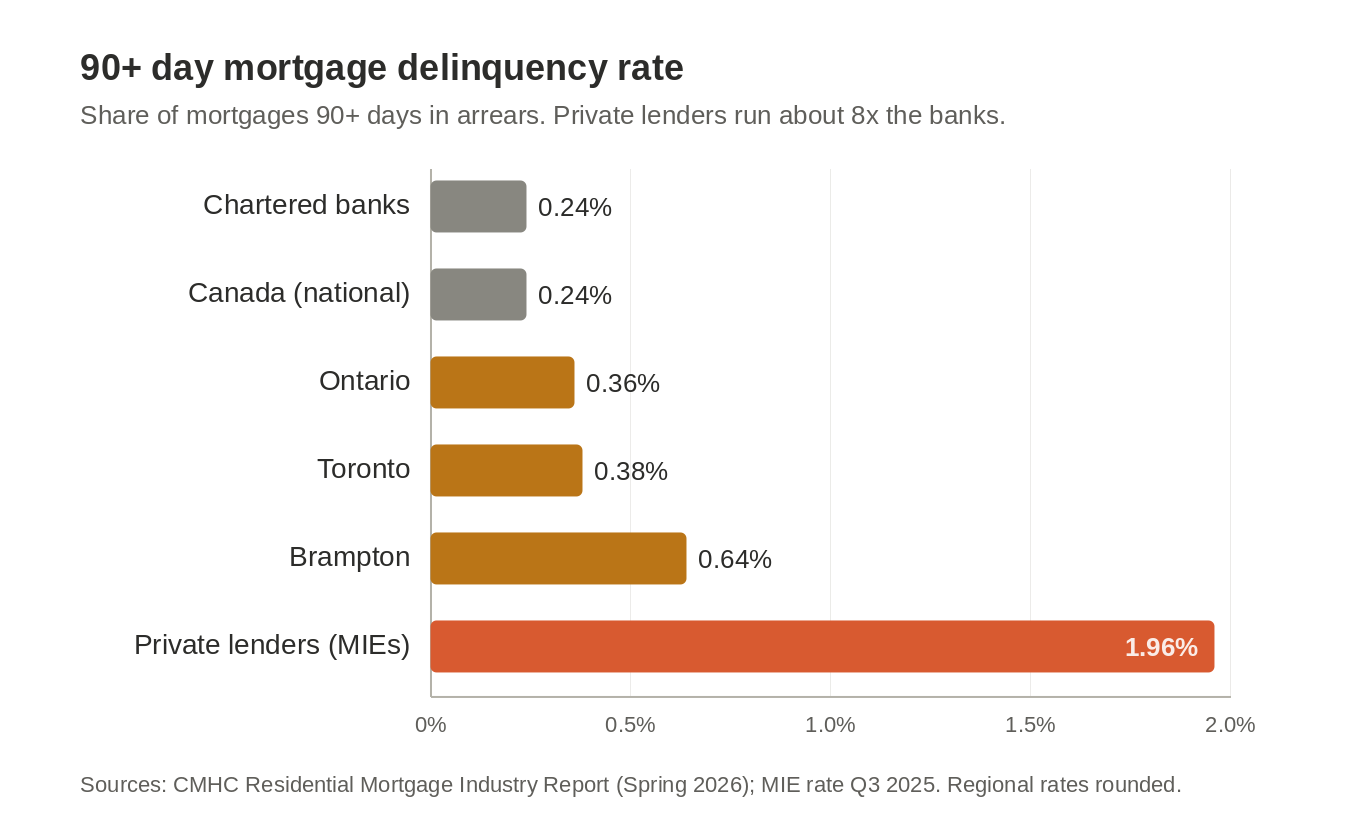

This is not happening in a vacuum. Mortgage trouble has been building across Ontario. According to CMHC’s Spring 2026 reporting, the national 90-plus-day delinquency rate reached 0.24% at the end of 2025 — the highest since 2019 — and Ontario has led the rise, around 0.36%, with Toronto near 0.38% and Brampton highest at roughly 0.64%. Among private lenders the strain is far sharper: delinquency at mortgage investment entities ran near 1.96% — many times the banks’ rate — though they hold only about 1% of all mortgages. And it shows up on the ground: active power-of-sale listings across the GTA were up about 59% year-over-year by late 2025, with more than 300 recorded across Ontario in a single month this past spring. Much of this traces to the “renewal cliff” — mortgages written at rock-bottom pandemic rates now renewing far higher.

So when more of these higher-risk mortgages go bad, more homes end up in power of sale. Ed’s borrower is not unusual — he’s a data point in a trend.

Now, the part that matters for your options. Banks operate inside a thick rulebook. Before a regulated lender puts a mortgage in front of you, it has to disclose the true cost of borrowing in a set way, spell out every fee, and consider whether the loan actually suits your situation. In Ontario, mortgage brokers and lenders are overseen by a provincial regulator — the Financial Services Regulatory Authority of Ontario — under rules meant to ensure borrowers understand what they’re signing.

Private lenders are supposed to follow much of the same playbook. But in a fast, high-pressure deal — borrower desperate, lender moving quickly — that’s exactly where steps get skipped. Disclosure that should have been clear gets buried. Fees that should have been explained aren’t. Independent advice the borrower should have received never happens.

And here’s the key point this whole article has been building toward: those skipped steps aren’t just paperwork. They can be the very things that give you leverage. That’s what we turn to next.

Can You Stop a Power of Sale in Ontario?

This is the question everyone asks first: how do I stop a power of sale in Ontario?

Here’s the honest answer. Usually, you can’t simply stop the sale. If you can pay out the mortgage — refinance, sell on your own terms, or cure the default within the redemption window — that’s the clean way out. Short of that, the lender is generally entitled to proceed.

But “you can’t always stop it” is not the same as “you have no leverage.” This is where my earlier point comes back. By the time a file like this reaches my desk, the sale is long over and I find myself wishing someone had asked the right questions while there was still time. So here they are — the questions a borrower, or the borrower’s lawyer, should be asking the moment a Notice of Sale arrives. Each one is a place where a private lender, moving fast, may have cut a corner. A cut corner is your leverage.

1. Was there one lawyer acting for both sides?

Start here, because it’s the strongest. In Ontario, Rule 3.4-12 of the Law Society’s Rules of Professional Conduct flatly prohibits a lawyer from acting for both the lender and the borrower on a mortgage. There’s a narrow exception for an institutional “lending client” — but a private mortgage lender or MIC is not a lending client within the meaning of the rule (Rule 3.4-13). So the exception doesn’t apply, and using one lawyer for both sides is a straight breach. If that happened on your file, it matters.

2. Did the borrower get real, independent legal advice?

Closely related. Independent legal advice (ILA) only counts if it was genuinely independent — not a lawyer the lender chose, steered you to, or rushed you through. The Law Society’s recent decision in Law Society of Ontario v. Baykara, 2026 ONLSTH 43 is a pointed example of what goes wrong in the private and syndicated mortgage world when ILA is inadequate, conflicts go unmanaged, and disclosure is incomplete.

3. Were the mortgage documents prepared correctly in the first place?

The validity and enforceability of the mortgage itself — and of the fees and penalty-interest structure built into it — is worth examining closely.

Ontario has a specific law on this. Mortgage brokers and lenders operate under the Mortgage Brokerages, Lenders and Administrators Act, 2006, and a regulation made under it called Ontario Regulation 191/08, “Cost of Borrowing and Disclosure to Borrowers.” In plain terms, that regulation says the lender’s side has to hand the borrower a written disclosure statement, in clear and plain language, before the borrower commits — generally at least two business days ahead. That statement must lay out the real, all-in cost of the loan, expressed as an annual percentage rate that folds the fees into the rate — not just the headline number on the front page.

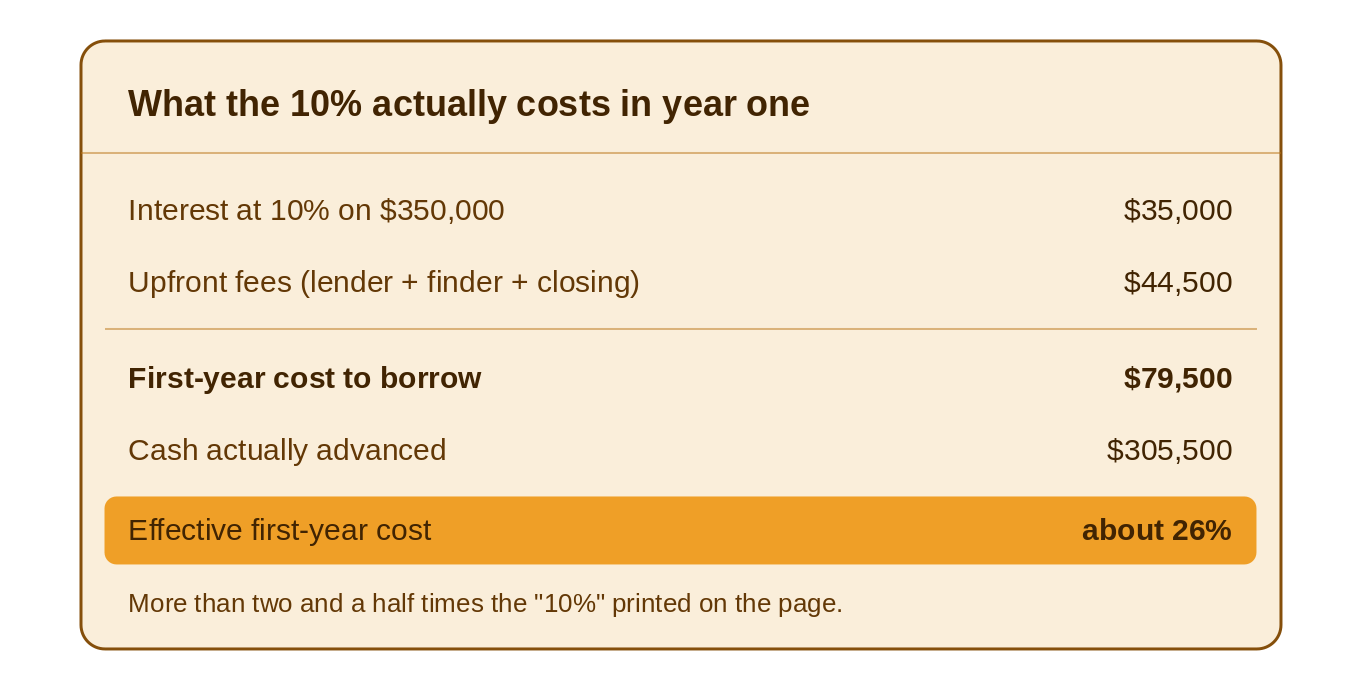

Think back to Ed’s loan. The page said 10%. The true first-year cost was closer to 26% once the fees were counted. The whole point of this disclosure law is that a borrower is supposed to be shown that real figure, clearly, with time to absorb it before signing. When that disclosure wasn’t given — or was buried, rushed, or simply skipped, as it often is in a fast private deal — it raises a real question about the enforceability of what the lender is now claiming. The regulator that oversees all of this is the Financial Services Regulatory Authority of Ontario, the provincial body responsible for mortgage brokering conduct.

4. Did the lender sell the home properly — in good faith and for true market value?

A lender exercising power of sale isn’t free to dump the property. It must act in good faith and take reasonable steps to obtain the true market value — it cannot conduct an improvident sale. That duty is well settled: see Dhaliwal v. Plantus, 2007 CanLII 46164 (ON SC) and, foundationally, J. & W. Investments Ltd. v. Black, 1963 CanLII 471 (BC CA). A sale rushed through below value is a sale you can challenge.

5. Does the deficiency actually add up — or is it a farce?

This is where my trustee’s eye goes — and it cuts both ways. Sometimes the lender claims a shortfall after the sale; sometimes it claims there was nothing left at all. Either way, every line of that accounting deserves scrutiny: the lender fee, the finder’s fee, default and penalty interest, placed-insurance charges, and so-called “protective advances.”

Start with the outer edge. I once dealt with a private lender that tried to bill private-investigator and surveillance fees as “recovery expenses” against what it was owed. That is the extravagant end of the spectrum, and it didn’t fly — costs added to a secured claim have to be reasonable, properly incurred, and authorized.

But the version you are far more likely to meet is quieter, and it is where real money is recovered. In one matter, a home was sold under power of sale by a private lender, and the lender’s discharge statement showed no surplus — in fact, a loss. On its face, the borrower walked away still owing money. A line-by-line reconciliation against the registered schedule to the charge told a very different story. Buried in the statement were:

- a “closed-mortgage penalty” that simply duplicated the three-month-interest default remedy the mortgage already provided;

- two full years of force-placed insurance, plus separate “placement” fees — on the order of $13,500 for roughly five and a half months of possession, where the real cost to insure was a fraction of that;

- a “contingency holdback” with no contractual basis;

- doubled NSF and statement fees; and

- enforcement legal fees charged twice — once as the lender’s administrative charge, and again as the solicitor’s own bill.

Each of those is a charge triggered by the borrower’s default — and that is exactly what brings it inside the law on penalties. A default-triggered charge is unenforceable as a penalty where the sum is “extravagant and unconscionable in comparison with the greatest loss that could conceivably be proved”: the test restated by the Court of Appeal in 660 Sunningdale GP Inc. v. First Source Mortgage Corporation, 2024 ONCA 252. Insurance billed at many times its real cost is the textbook example. That same case is a caution, not a shield — it upheld a lender’s fee precisely because the fee was not triggered by any default, the very distinction that decides these disputes. And unauthorized charges piled onto a secured claim can be struck outright: Dhaliwal v. Plantus, 2007 CanLII 46164 (ON SC).

Once those charges came out, the “loss” became a surplus — and roughly $25,000 that the statement said did not exist was paid back into the borrower’s insolvency estate.

Here is the part worth underlining: you do not need to be in a bankruptcy or a proposal to do this. Any borrower, or the borrower’s lawyer, can demand the full payout statement, ledger, invoices, listing agreement, statement of adjustments and commission statement, then reconcile each charge against the mortgage and the schedule to the charge. The right to a proper accounting — and to any surplus — is the borrower’s. Insolvency simply adds standing and leverage: a direction of the net proceeds, and a certificate registered on title that the lender must clear before it can close.

One boundary belongs in this story. When a Licensed Insolvency Trustee acts as the administrator of a consumer proposal, the trustee has to tread more carefully than in a bankruptcy — because the assets are not the trustee’s to control. In a bankruptcy, the debtor’s property vests in the trustee under section 71 of the BIA, and the trustee deals with it in its own right. In a consumer proposal, nothing vests: the home, and the proceeds of its sale, remain the debtor’s. The administrator’s role is to protect the integrity of the proposal the debtor filed — here, the term requiring the net proceeds to be paid in — not to act as the debtor’s lawyer.

That line matters in practice. In the matter above I was careful to say, in writing and more than once, that I was not counsel for the borrower, that my comments were not binding on her, and that the final decision to settle — a decision about her own assets — was hers to make, with her own lawyer if she chose one. A trustee-administrator who slides from protecting the proposal into advising the debtor on her legal rights has overstepped the role. The discipline is to do the forensic accounting, surface the issues, press the lender — and leave the call to the person whose property it still is.

So: can you stop a power of sale in Ontario? Often, not the sale itself. But you can hold the lender to account on every one of these points — and that accountability is exactly what shapes what you owe at the end, and what your options are if insolvency does come into play.

Can filing with a Licensed Insolvency Trustee pause a power of sale? (the stay)

This is usually the next hope: if I file a consumer proposal or a bankruptcy, doesn’t that freeze everything — including the power of sale?

It’s a fair assumption, because filing does freeze a great deal. The moment you file with a Licensed Insolvency Trustee, an automatic protection called a stay of proceedings snaps into place. It stops most creditors in their tracks — the collection calls, the lawsuits, the wage garnishments. For unsecured debt, the stay is powerful.

But a mortgage is different, and this is the part people are surprised by: a stay generally does not stop a secured lender’s power of sale. (see note below)

Here’s why, in plain terms. (The section numbers below refer to Canada’s Bankruptcy and Insolvency Act — the federal law that governs proposals and bankruptcies. We’ll call it the BIA.)

When you file, a stay stops your creditors from collecting unsecured debts — the claims that get proved and paid through your insolvency. The stay arises under section 69.2 of the BIA in a consumer proposal and section 69.3 in a bankruptcy.

But a mortgage is different. The lender’s claim is tied to your house, not to the pool of money shared among unsecured creditors. So the power of sale is not caught by the stay at all. Filing a consumer proposal does not pause the mortgage proceedings — and neither does filing for bankruptcy. The lender can carry on.

What the stay does reach is the lender’s pursuit of the shortfall — the money you would still owe after the house is sold for less than the debt. That shortfall is an unsecured claim, and that is the piece your insolvency stops the lender from chasing you for directly.

So what does filing accomplish here? It changes the shape of the lender’s claim. Once the home is sold and the proceeds fall short, the lender no longer holds the whole hammer. That shortfall — the deficiency — becomes an ordinary unsecured claim in your insolvency, ranking alongside your other unsecured creditors rather than chasing you personally without limit. The mechanics live in the Act: a secured creditor proves its claim and values its security (sections 127 and 135), contingent or valued amounts are dealt with (section 121(2)), and everything ranks for distribution under section 136. The same logic applies inside a consumer proposal — the secured shortfall is treated as unsecured.

In other words: filing usually won’t save the house from a power of sale already in motion. What it does is contain the fallout — converting an open-ended personal pursuit into a defined, ranked claim handled through the insolvency.

One timing trap worth flagging. A debtor who files but stays living in the home afterward can face a claim for occupation rent — essentially a charge for the use of the property during that period. It’s an equitable, fact-dependent question, and the amount is never automatic. Don’t assume a number; this is one to work through with your trustee and, where needed, counsel.

Even after you file, the lender may keep pursuing you (inspectors)

There’s one more move an aggressive private lender can make, and most people have never heard of it. To understand it, you need to know what an inspector is.

When someone files a bankruptcy, the creditors can appoint inspectors — usually one to five of them — to oversee the trustee’s work on the creditors’ behalf. Think of an inspector as a supervisor representing the creditor group: they approve certain decisions, review the trustee’s handling of assets, and have real influence over how the estate is administered. The role exists to protect creditors as a whole.

Here’s the problem. An aggressive lender — the same one that just put your home through power of sale — may try to become an inspector itself, to steer the bankruptcy from the inside and protect its own position. That is exactly what the law guards against.

The conflict rule. Under section 116(2) of the Bankruptcy and Insolvency Act (the BIA), a creditor who is a party to a contested matter with the estate cannot serve as an inspector. The leading recent statement is Re The Aggressive Good Inc., 2025 ONSC 1419, which sets out the modern test: a creditor is barred whenever such a conflict exists — whether it was there at the start or arises later — and the standard is actual or even perceived conflict with the inspector’s duty to the creditors as a whole. Supporting authorities run the same way: Global Plastic Packaging, 2004 CanLII 16817, and, in Ontario, Re Canadian Triton International Ltd., 1997 CanLII 12412 (ON SC) (Farley J., who observed — in obiter — that a creditor whose own claim is contested has “questionable” eligibility), along with Re Wimco, 1970 CarswellOnt 84.

When a lender is clearly disqualified. A lender that is tied up in contemplated preference or recovery proceedings — where the estate may go after transactions involving that lender — is ineligible to act as inspector. See BGA Financial Group Inc. (Syndic de), 2016 QCCS 5870.

The honest other side. This doesn’t mean every secured lender is disqualified. Ordinary, garden-variety enforcement of a security does not by itself bar a creditor from serving as an inspector — Morrison v. Toronto-Dominion Bank, 1980 CanLII 1149 (AB QB); 9333-8309 Québec inc. c. Houshmand, 2021 QCCS 4414. The line is drawn at conflict, not at simply being a secured creditor.

Your lever as the debtor. Here’s a point worth knowing: in rare but appropriate cases, the debtor itself can apply to have a conflicted inspector removed — you are not purely a bystander. The origin of the rule that section 116(2) reaches even a corporate creditor’s representative who is in litigation with the estate is Re Promédia Inc. (also reported as Maheu v. Rodrigue) (1984), 51 C.B.R. (N.S.) 132 (Que. S.C.).

The trustee’s own tools. A trustee is not powerless against aggressive pre-bankruptcy grabs, either. The BIA lets the estate unwind certain transactions — sections 95 and 96 deal with preferences and transfers at undervalue, and section 4 presumes parties were not dealing at arm’s length in defined relationships, which makes some of those transactions easier to challenge.

Inflated or unauthorized charges added to a secured claim are vulnerable in the same way — as the recovery example earlier in this article shows. The governing principle is simple: costs added to a secured claim have to be reasonable, properly incurred, and authorized, and they are open to scrutiny by the trustee and the court. Dhaliwal v. Plantus, 2007 CanLII 46164 (ON SC) disallowed unauthorized fees on exactly that logic, and the valuation of a secured claim under section 135 of the BIA is where that scrutiny happens.

All of this sits on a foundation written into the role of every trustee: under section 13.5 of the BIA and General Rule 39 of the Code of Ethics, trustees must be honest and impartial. The system is built so that no single aggressive creditor gets to capture it.

If you’re early in the story, use the time

Come back to where we started. By the time most of these files reach my desk, the house is gone and all that’s left is a letter telling someone how much they still owe. From that seat, I keep wishing I could turn back the clock — because so often, the questions that mattered were never asked while there was still time to ask them.

If you’re reading this earlier in the story — a Notice of Sale freshly in hand — you have something those later files didn’t: time. Use it. Before you conclude that bankruptcy or a consumer proposal is your only road, work through the questions in this article. Was there one lawyer for both sides? Was the independent legal advice real? Was the cost of borrowing properly disclosed? Was the sale conducted in good faith and for true market value? Does the deficiency actually add up? Each answer can change where you end up.

Insolvency is a genuine tool, and sometimes it is the right one — but it should be a considered decision, not a panic reflex. If it does turn out to be the right path for you, that’s something I can help with.

For borrowers: if a private mortgage lender has started a power of sale on your home, don’t assume the outcome is fixed. Get advice early, while the redemption window is still open.

For lawyers, brokers, and other advisors: the accountability checklist above is where files are won or lost. If you’re advising someone in this position, these are the questions to run down first.

Note:

A technical note for completeness. One form of filing — a Division I proposal — can be structured to include, and even bind, secured creditors such as mortgage lenders. But actually staying a secured mortgage lender this way is rare in the consumer world. It’s a more involved restructuring strategy seen mainly in corporate insolvencies, where secured lenders themselves can sometimes come out ahead through the restructuring. For an ordinary consumer mortgage, a debtor pursuing that remedy would be very unusual — which is why the general rule above holds in practice.

GET IN TOUCH WITH PAUL

TURN CRISIS INTO OPPORTUNITY

When you’re ready to see your debt options clearly, the light is on.